The appointment went well. The crown looks beautiful and fits perfectly. Then the insurance Explanation of Benefits arrives — and the number is lower than expected. A larger balance remains on the patient's statement than they anticipated. The first thought, completely understandably, is that the dental office charged too much. That instinct is wrong — not because the patient is wrong to question it, but because the insurance company has made a decision that has nothing to do with what the dentist charged. Understanding the difference changes everything.

Two Separate Questions That Get Confused as One

When patients see a higher-than-expected balance after a crown, they are actually looking at the answer to two different questions collapsed into one number. The first question is: what did the dentist charge for the crown? The second is: what did the insurance company decide to pay? These are independent decisions made by independent parties — and when the balance is larger than expected, it almost always traces back to the second question, not the first.

"Insurance paid less than I expected — so the dental office must have charged more than they should have."

✗ What patients assume

- The dentist charged for a premium material and padded the bill

- If insurance paid less, that means the dentist is overcharging

- A lower insurance payment means the procedure was overpriced

- The office could have chosen a cheaper option and saved me money

- My plan covers crowns — so this should have been mostly covered

- The office billed the wrong code and that's why the payment was low

- Insurance only pays what's "reasonable" — and this wasn't

✓ What actually happened

- The insurance applied an Alternate Benefit Provision — a policy term

- The insurer chose to pay at the rate of a cheaper material — not the one placed

- The dentist's fee for a porcelain/zirconia crown is the market rate for that material

- The material was chosen on clinical grounds — biocompatibility, durability, anatomy

- Your plan may cover crowns but limit payment to the cost of a metal crown

- The code was correct — the insurer simply pays at a different code's rate

- "Reasonable" is defined by the insurance company's fee schedule, set internally

What the Alternate Benefit Provision Actually Is

Most patients have never heard of the Alternate Benefit Provision — also called the Least Expensive Alternate Treatment (LEAT) clause — but it is one of the most common reasons a dental bill ends up higher than expected after insurance. It is written into the majority of dental PPO contracts in America. Understanding it takes about two minutes, and it will change how you read every dental insurance Explanation of Benefits you ever receive.

The clause works like this: when two or more clinically acceptable treatments exist for a condition, the insurance company will pay based on the cost of the least expensive option — regardless of which treatment was actually provided. If you receive a porcelain crown and the insurance company considers a metal crown an acceptable alternative, they pay at the metal crown rate. The difference between the metal rate and the porcelain rate becomes part of your patient balance — not because the dentist charged too much, but because the insurance company exercised a contractual right it reserved before you ever enrolled.

The Math in Real Numbers: Where the Gap Comes From

The best way to make this concrete is to walk through the actual numbers. Here are two real scenarios — one with a posterior (back) tooth and one involving a front tooth — showing exactly where the patient balance originates and why none of it is the dental office's fee decision.

Patient needs a crown on tooth #30 (lower right molar). Dr. Nguyen places a zirconia crown — metal-free, strong enough for molar forces, biocompatible. Insurance policy contains an alternate benefit provision: posterior crowns paid at full metal rate only.

Patient has decay on a back molar. Dr. Nguyen places a tooth-colored composite resin filling — clinically preferred, mercury-free, bonds to tooth structure. Insurance policy applies a composite downgrade: posterior fillings paid at amalgam (silver) rate.

Why the Material Was Chosen — It Was Never About Cost

The most important thing to understand about a crown material recommendation is that it begins — and ends — with the patient's clinical situation. Dr. Nguyen is not choosing materials based on fee schedules, insurance allowables, or what produces the highest bill. Here is what actually drives the material decision for every crown placed at SoftDental.

(Insurance pays this)

(Anterior / visible)

(Posterior / high-force)

The Decision Chain — Who Controls What, in Order

Every crown involves a sequence of decisions made by different parties. When the final bill looks higher than expected, it helps to trace which decision belongs to whom. Most patients discover the gap is almost entirely in steps they did not control.

🔬 Clinical Diagnosis

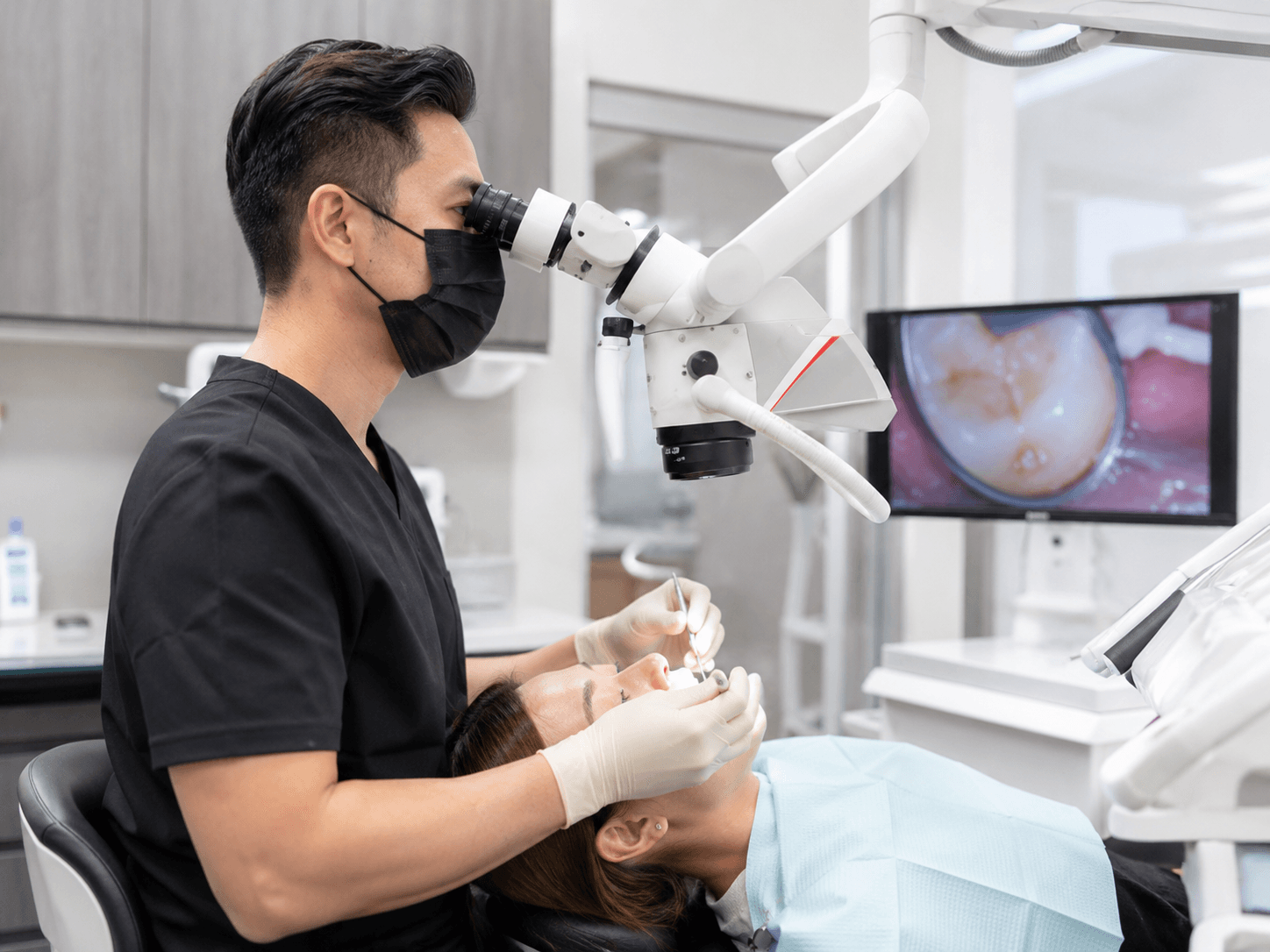

Dr. Nguyen examines the tooth using X-rays, periodontal probing, and direct visual inspection — often under the Leica M320 microscope for fine margin evaluation. The diagnosis determines that a crown is clinically necessary. This is not a billing decision. It is a clinical judgment driven by the condition of the tooth.

Dental office decides🦷 Material Selection

Based on the tooth's position, the bite forces it experiences, the patient's history of grinding, the esthetic zone requirements, and any metal sensitivity concerns, Dr. Nguyen recommends a specific crown material. For most patients in 2026, this is eMax for front teeth and zirconia for back teeth. Both are metal-free, biocompatible, and long-lasting. The patient's informed consent is obtained before any treatment begins.

Dental office recommends Patient consents💵 Fee Setting

The dental office sets its fee for the procedure based on actual costs: lab or milling costs, materials, chair time, clinical staff time, overhead, and the complexity of placement. This fee is the same for every patient receiving that procedure — it does not change based on which insurance the patient carries. The fee is set by the practice, not by the insurance company.

Dental office sets📋 Insurance Payment Decision

The dental office submits the claim with the correct CDT code for the material placed. The insurance company then reviews the claim against the terms of the contract — the one the patient's employer purchased. If the plan has an alternate benefit provision, the insurer applies it and pays at the lower material rate. This decision is made entirely within the insurance company's offices. The dental team has no part in it. The dental office also cannot tell the insurance company which code to pay at — that is determined by the policy terms, not by the claim submission.

Insurance company decides🧾 Patient Balance

The patient balance is the dentist's fee minus what insurance paid. When insurance applies a downgrade, the balance is higher than the patient expected — because the insurer paid less than the procedure actually cost. This is not an overcharge. It is the mathematical result of a policy the insurance company wrote before the patient ever walked into this office.

Patient receives billWhat We Control — And What We Genuinely Cannot

Clinical Diagnosis and Material Recommendation

Dr. Nguyen determines what treatment is needed and which material is clinically appropriate. This is the core of dental care and will always be driven by what is best for the patient's tooth — not by insurance payment rates.

Accurate CDT Coding and Same-Day Claim Filing

We submit the correct procedure code for the material placed, with all supporting documentation — X-rays, clinical notes, photographs. Claims are filed the same day of service. Coding errors are one area where the office is responsible — and we take it seriously.

Pre-Authorization and Benefit Verification

Before major treatment, we submit pre-authorization requests and verify your benefits — including checking whether an alternate benefit provision applies to your specific plan for the planned procedure. We tell you in advance if a downgrade clause exists.

Filing Appeals With Clinical Evidence

When a downgrade is applied and there is clinical justification to challenge it — such as documentation showing why a metal crown is not appropriate for this specific patient — we build the appeal and file it. This costs time we do not bill for.

What Your Insurance Policy Says

The alternate benefit provision was written by your insurance company and accepted by your employer before you enrolled. We did not write it, sign it, or negotiate it. We cannot change it.

The Amount Insurance Decides to Pay

The insurance company's payment amount is determined by their fee schedule and your plan's terms. These are set internally by the insurer. We receive the payment amount on the Explanation of Benefits just like you do — after the fact.

The Insurance Company's UCR Fee Schedule

The "Usual, Customary, and Reasonable" rates that limit insurance payments are set by the insurance company. The ADA itself passed a resolution in 1997 recommending insurers stop using the term because it implies the dentist's fee is unreasonable — which it does not. The UCR rate is simply the insurance company's internal ceiling, not an external market benchmark.

Whether an Appeal Will Be Approved

We file appeals when appropriate and supported by clinical evidence. But the insurance company makes the final decision on every appeal. If the alternate benefit provision is written into your contract and the insurer upholds it, no amount of documentation will reverse it. The contract is the contract.

If You Believe a Downgrade Was Applied: What You Can Do

A downgrade is not always final. In some situations — particularly where clinical documentation clearly shows why the alternate material was not appropriate — appeals can succeed. Here is a practical path forward.

Read Your Explanation of Benefits Line by Line

The EOB is the document your insurance company sends after processing a claim. It shows exactly what procedure code was billed, what code they paid at, what amount they allowed, and what percentage they paid. If you see a different procedure code in the "paid" column than the one that was billed — that is the downgrade in writing. This document is the starting point for any conversation.

Call Your Insurance Company and Ask Them to Explain the Downgrade

Ask specifically: "Your EOB shows you paid at code D2710 but my dentist billed code D2740. Can you explain why a downgrade was applied and what my plan's alternate benefit provision says about posterior crown materials?" Write down the representative's name, the call date, and what they tell you. This is your insurance policy — you are entitled to a full explanation.

Ask Our Office to Check Whether an Appeal Is Supported

Bring the EOB to us, or call and ask us to review the claim. We will look at whether the downgrade was applied correctly under your plan terms, and whether clinical documentation — such as evidence of metal sensitivity, limited occlusal space requiring a specific material, or other documented clinical necessity — supports an appeal. We will tell you honestly whether an appeal is likely to succeed. We will not file an appeal just to run out the clock on your behalf if the policy language is clear.

If an Appeal Is Filed, Provide Any Supporting History You Have

If you have documented metal allergies, previous reactions to dental metals, or other relevant medical history, provide that to us to include in the appeal. Insurance companies are more likely to reverse a downgrade when the clinical reason for selecting the non-downgraded material is clearly documented and patient-specific — not just a general preference.

For Next Time: Ask About Downgrade Clauses Before Treatment

Before major restorative work, ask our insurance team: "Does my plan have an alternate benefit provision for this procedure? If so, what material does it pay at, and what will my estimated balance be?" We verify benefits before every appointment. This question takes two minutes to ask and can prevent every surprise you have ever had on a dental bill.

When a patient gets a bill that is higher than they expected, my first instinct is compassion — not defensiveness. I know it feels like something went wrong. What I ask for is two minutes to explain exactly what happened. Almost every time, the conversation ends with the patient understanding that their insurance company made a financial decision — and that our office has been on their side from the start. We always will be.

— Dr. Minh Nguyen, D.D.S., P.A. · SoftDental, Houston TX · MCXL Same-Day Crowns · eMax · Zirconia · Leica M320 MicroscopeGot a bill that doesn't make sense?

Call us before you assume the worst. Our insurance team will walk through the EOB with you, explain exactly what happened, and tell you honestly whether an appeal is worth filing.

Educational content only. Insurance plan terms, alternate benefit provisions, procedure codes, fee schedules, and payment amounts vary significantly by plan and insurer. The scenarios presented use illustrative numbers — actual fees and insurance payments will differ by plan, location, and provider. Always verify your specific plan terms with your insurance company before major treatment. CDT code information current as of 2025 ADA Current Dental Terminology. UCR history citation from ADA 1997 resolution. © 2026 SoftDental | Dr. Minh Nguyen DDS PA · 10028 West Road Ste. 108, Houston TX 77064 · 281-807-6111